Eco (Atlantic) Oil & Gas – Good read across from Kawa-1 well in offshore Guyana

![]()

By Dr. Michael Green

There is little doubt that Eco (Atlantic) Oil & Gas is currently exploring for hydrocarbons in some global hotspots – offshore Guyana, offshore Namibia and offshore South Africa.

It has just been announced today that the Kawa-1 well in offshore Guyana has encountered 177 feet (54m) of hydrocarbon bearing reservoirs based on logging while drilling. This latest discovery from offshore Guyana was announced by CGX Energy and Frontera Energy Corporation – joint venture partners in the Petroleum Prospecting Licence for the Corentyne Block.

The Kawa-1 well encountered 177 feet of hydrocarbon-bearing reservoirs within Maastrichtian, Campanian and Santonian horizons. The JV partners were quick to point out that these intervals are similar in age and can be correlated using regional seismic data to recent successes in Block 58 in Suriname and Stabroek Block in Guyana. The Kawa-1 well was drilled to a depth of 21,578 feet (6,578m) and targeted the easternmost Campanian and Santonian channel/lobe complex on the northern section of the Corentyne block.

At the time Gabriel de Alba, Chairman of Frontera’s Board of Directors and Co-Chairman of CGX’s Board of Directors comment that “Initial results from the Kawa-1 well are positive and reinforce CGX and Frontera’s belief in the potentially transformational opportunity our investments and interests in Guyana present for our companies and the country. Kawa-1 results add to the growing success story unfolding in offshore Guyana as the country emerges as a global oil and gas exploration hotspot….”

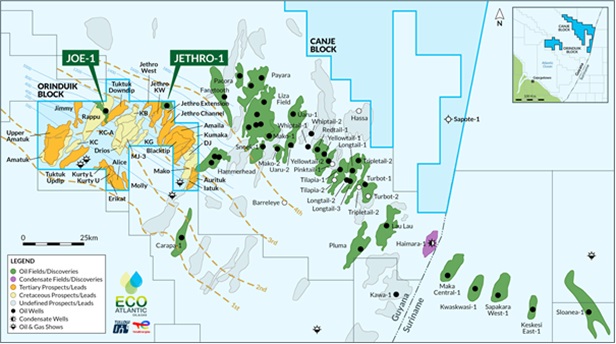

Map of the offshore Guyana Orinduik Block highlighting the position of the Kawa-1 discovery.

Source: Company

This discovery marks the first find outside of Stabroek. It is the same play, same trend, same thickness and same slope. There is a clear trend of discoveries from NW to south which is awfully good news for Eco which in partnership with Tullow Oil and TotalEnergies/Qatar Petroleum, where the company holds a 15% working interest in the 1,800km² Orinduik offshore block in the shallow to medium depth water of the prospective Guyana-Suriname basin.

Eco’s licence area is adjacent to ExxonMobil’s multiple world class discoveries on the Stabroek Block where recoverable resources of more than 10 billion barrels of oil have been estimated. First production began in late-2019 from the Liza Field. In 2019, Eco was able to announce a significant oil discovery on the Orinduik Block from the Jethro-1 exploration well. The discovery has been estimated to contain over 100 million barrels of oil – above the pre-drill estimates, and followed by a further discovery at the Joe-1 exploration well. June 2021 also saw Eco acquire up to a 10% interest in JHI which has a 17.5% working interest (WI) in the ExxonMobil-operated Canje Block.

Eco first started trading on the TSX-V in 2011 with Namibian oil interests. Progress was quite rapid and by 2016 the company teamed up with Tullow to acquire a licence in Guyana to explore similar basins in the margins on the other side of the Atlantic Ocean, ahead of becoming dual-listed in 2017. The shares climbed to 190p plus in 2019 following the drilling of two discovery wells in Guyana which confirmed the prospectivity of the upper and lower Tertiary fairways. News that the wells contained sour heavy oil disappointed the market and the share price plunged. Truth is that since that time the stock has remained a bit unloved.

June/July 2022 could see Eco’s partners in the Orinduik Block unveiling a decision to resume drilling into light oil Cretaceous targets, the source of ExxonMobil’s huge success on the adjoining Stabroek Block where the 120,000 bopd Liza Field went into production in late 2019, following discovery in 2015. The Liza Oil field is about to see production being given a massive boost with Phase Two Development this year which will increase the total production capacity to 340,000 boed.

At the same time there are plenty of potential catalysts for wider regional success in SA and Namibia, with the market eagerly awaiting confirmation of recent rumours concerning offshore Namibia which have been swirling around. Eco’s strong strategic positioning in Namibia could rapidly become more valuable if rumours that Shell has discovered light oil at its Graff-1 exploration well are true.

We believe that Namibia could become one of the hottest global oil & gas plays – so a good time for Eco to have recently upped its interest by acquiring Azinam. This deal also adds two South African Orange Basin blocks, Block 3B/4B, that are directly correlated to Graff-1 and Block 2B, a shallow water block with previous light oil discovery. A potential success of either Graff-1 or Venus-1 or both would be transformational for Namibia and would be big potential catalysts for wider regional success.

We recently updated our research coverage on Eco with a Conviction Buy stance and a target price of 114.65p. At the current price of 28p, we are more than happy to confirm our stance.

RISK WARNING & DISCLAIMER

Eco (Atlantic) Oil & Gas is a research client of Align Research. Align Research holds an interest in the shares of Eco. Full details of our Company & Personal Account Dealing Policy can be found on our website http://www.alignresearch.co.uk/legal/

This is a marketing communication and cannot be considered independent research. Nothing in this report should be construed as advice, an offer, or the solicitation of an offer to buy or sell securities by us. As we have no knowledge of your individual situation and circumstances the investment(s) covered may not be suitable for you. You should not make any investment decision without consulting a fully qualified financial advisor. Align Research is bound to the company’s dealing policy, ensuring open and adequate disclosure. Full details can be found on our website here (“Legals”).

Your capital is at risk by investing in securities and the income from them may fluctuate. Past performance is not necessarily a guide to future performance and forecasts are not a reliable indicator of future results. The marketability of some of the companies we cover is limited and you may have difficulty buying or selling in volume. Additionally, given the smaller capitalisation bias of our coverage, the companies we cover should be considered as high risk.

This financial promotion has been approved by Align Research Limited